You may be reading this, trying to find the “best time to buy”. If so, maybe it’ll be your first home so you’d like to be cautious. Or perhaps you're thinking about purchasing an investment property, and you’d like to maximize your ROI by minimizing the purchase price.

Another possibility is that you are one of the 6400 (or so) people who bought in the period 2011-2014 and your goal is to sell your home, but can’t right now (or won’t). You may be hoping for prices to rise above today’s levels so that you can sell and settle your mortgage pay-out balance. For this to happen, prices would need to stop falling, balance out, and then go up, possibly for quite some time.

In either case, you probably want to know when the Fort McMurray housing market balances out (that is, when prices have stopped falling).

And it will. All markets balance.

Eventually.

I am writing this post so that you can get a sense of how housing markets work and what signs to expect that will signify that the market is indeed balancing (when prices are no longer falling).

If you haven’t yet read our blog “Fort McMurray Real Estate Crash: A Timeline”, doing so will get you up to date before reading on.

How Housing Markets Work

How do we know that the market will eventually balance? Well, it’s the central result of the most basic economic model: Supply and Demand...

As prices fall, there are fewer sellers willing/able to sell, and there are more buyers willing/able to buy (in a given time period). This, in turn, causes inventory to fall and transactions to increase. Eventually, there is the “Goldilocks” number of motivated buyers and sellers in the marketplace (remember the porridge - not too hot, not too cold), and prices stop falling. Regardless of what you may read elsewhere, please note that THAT is how supply and demand works.

However, housing markets are different to

financial markets in that it’s not just about money.

On the contrary, most housing decisions are about people’s lives; the majority of buying and selling decisions are a result of people attempting to select a primary property that fits their lifestyle. Over their lifetimes, individuals’ and families’ needs change and they exchange properties. Having a suitable roof over one’s head tends to be the driving factor in what property types people demand and when. This makes the market work a little differently from other markets.

Another strange thing about housing markets is that prices are really “sticky”. They lag events in the wider economy, primarily because, unlike in financial markets, money doesn’t wholly determine decisions (as noted above). Another reason is that that real estate is not as liquid as other assets - it takes time for people to gather information (which isn’t easily available) and the selling process is more complex than say, selling a Suncor share.

The idea of “sticky prices” is important because it gives us a window through which we can see that outside events might impact a family’s ownership decision months or years after the event itself.

This part is important, too:

Families’ budgets and risk tolerances vary because they are impacted by factors outside of their control. For example, elements like government policy, interest rates, wages, fear of unemployment, actual unemployment, etc. Moreover, those changes tend to happen to lots of households at the same time.

Now we can see that outside events tend to later impact:

a) The number of homes demanded

b) The types/price ranges of homes demanded

So that’s demand. What about supply?

Well, this is also determined by families, as well as firms, who develop raw land into lots (developers) and lots into homes (builders) in order to make profit. It is also impacted by natural disasters. The supply side is really a whole other topic, so, for now, I’ll make the assumption that most of the events of the last few years have impacted the demand for homes, not the supply of them.

Let’s explore how the factors above (total demand and distribution of demand) have changed as a result of recent events...

Total Demand

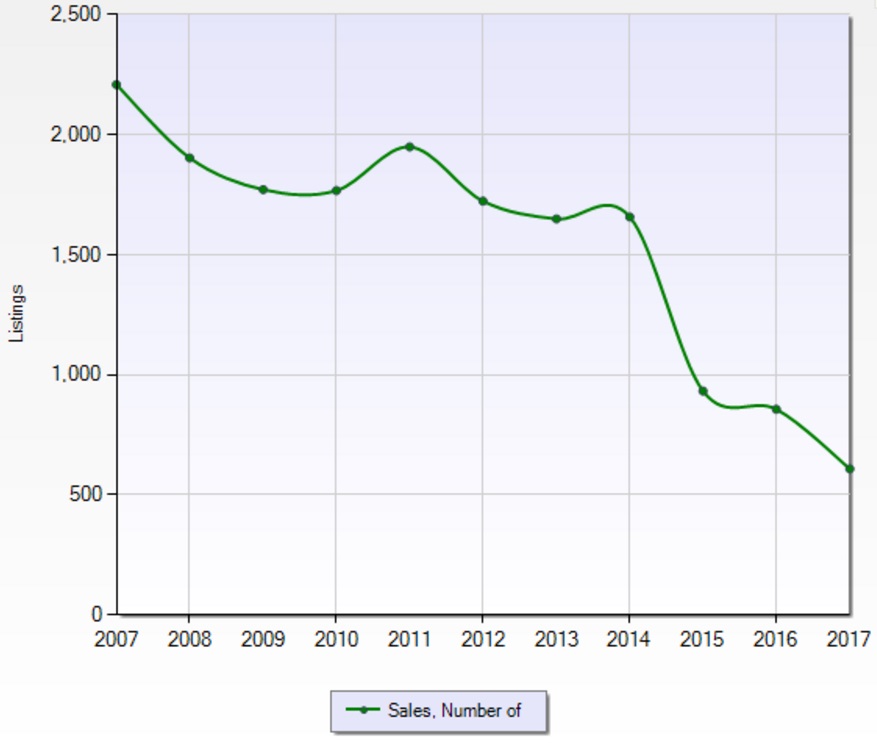

Here’s a chart

:

N.B. The 2017 datapoint is year-to-date (it will end the year higher, though most transactions for the year are behind us).

The striking conclusion from this chart is that transactions are still running at approximately a 45-50% slower rate than during the boom years. This is despite prices falling significantly. The impact of the oil shock, government policy changes, and the fire have had real, lasting impacts on families, and therefore on the demand for homes at a given price.

We would likely need to see a real sustained uptick in the rate of homes selling. We will explore this in more detail later.

Distribution of Demand

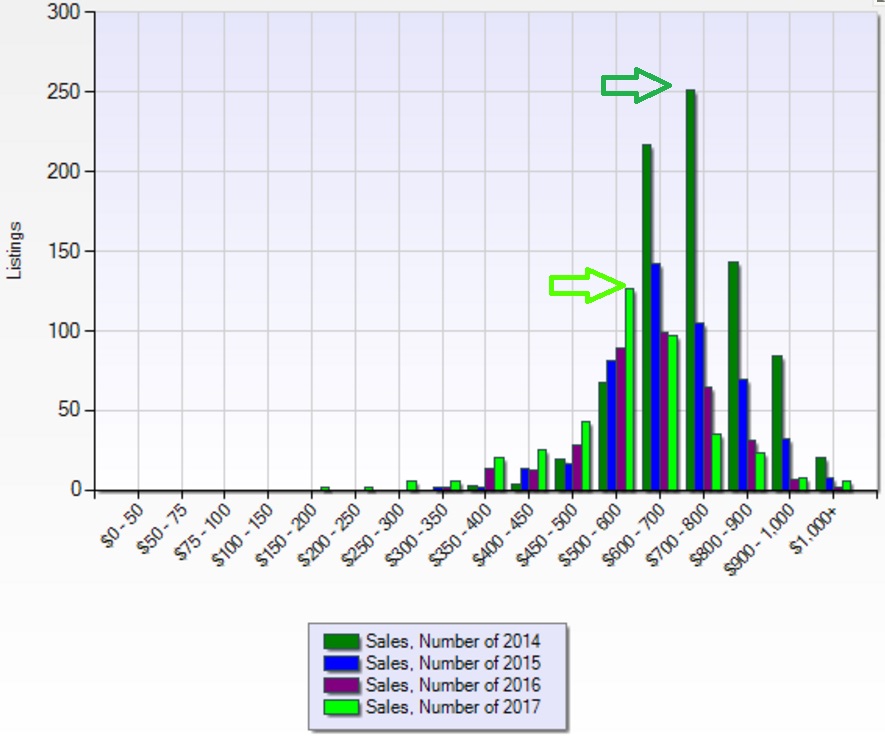

Here’s a histogram that shows the breakdown of sales over the different price ranges in each of the last four years (year-to-date)

:

The way to read this chart is just to look at each one of the colours at a time. For example, you can just look at 2014 sales by only looking at the dark green bars. Transactions that year were most commonly in the $700k-$800k price range (follow the dark green arrow).

As the years have gone on, the shape of demand has remained the same (it is shaped like a bell), but that the peak has moved down and sideways. The bright green arrow shows that the most common sale price in 2017 is now in the $500k-$600k price range. Further, it is about half as high as the peak in 2014. This reflects the lower total demand as noted in the previous section.

Let’s explore this a little bit.

Three years ago, the profile of a typical first-time buyer client of ours was as follows:

- Down-payment: 5%

- Bank’s budget (pre-approval): $800,000

- Personal budget: $750,000

- Property type: Prefers rental income from a basement suite

- Risk tolerance: High

- Works: At site

A lot has changed in the last three years. Our community has dealt with a lot. Without going into too much detail (we’d rather not think about it), let’s just say that a lot of families have been impacted significantly by the decisions of firms and governments near and far, as well as by natural disaster.

Therefore, today a “typical” first-time buyer of ours has the following profile:

- Down-payment: 15%

- Bank’s budget (pre-approval): $600,000

- Personal budget: $500,000

- Property type: Entry-level1

- Risk tolerance: Low

- Works: Maybe at site, maybe in town

This anecdotal evidence is very much in line with the charts and the theory. The next question is…

What Next?

We’re not allowed to attempt to forecast the market, but we do have an idea of what the next phase might look like, whenever the heck that is: We know prices won’t fall forever.

Prices could stop falling because of higher sales or because of fewer listings in a given time period or (most likely) both.

When prices do stop falling (or are about to), how will you know? In the absence of MLS® data, what signs can members of the public look out for? Which will be the earliest signs? Which will be the most reliable?

Signs of Recovery

1) Jobs, Jobs, Jobs

(And I’m not talking about Steve Jobs.)

Something that usually pre-empts recoveries in demand for housing is jobs. They don’t have to well-paying jobs, but they do need to be local and stable. While the rebuild is huge for the Alberta economy, it’s arguable that the rebuild hasn’t provided many stable, local jobs. Many of the workers are from out of town, and the rebuild is considered a 1 to 4-year event. Anecdotally, we only have one client who has come up for the rebuild and who is buying.

We are starting to see more jobs in town and there are rumors of more at site. Several of our buyer clients right now, for example, work for bus companies or nonprofits, or own their own businesses that they have started up since the cost of commercial space has come down.

So one thing to look for is stable jobs, and lots of them! After that, it’s only a matter of time before those employees save up and buy homes. Don’t just look for them in the news, watch for your job-seeking friends as they all start getting snapped up.

2) Smart People Buying Investments

The “smart money” usually moves in at just the right time.

Your buddy might be buying his first investment property, but it doesn’t mean it’s the perfect time. He’s more likely to be early than late.

What you want to watch for is the “smart money”. People from out of town, foreign buyers, wealthy, experienced locals, companies. These people might start purchasing multiple properties.

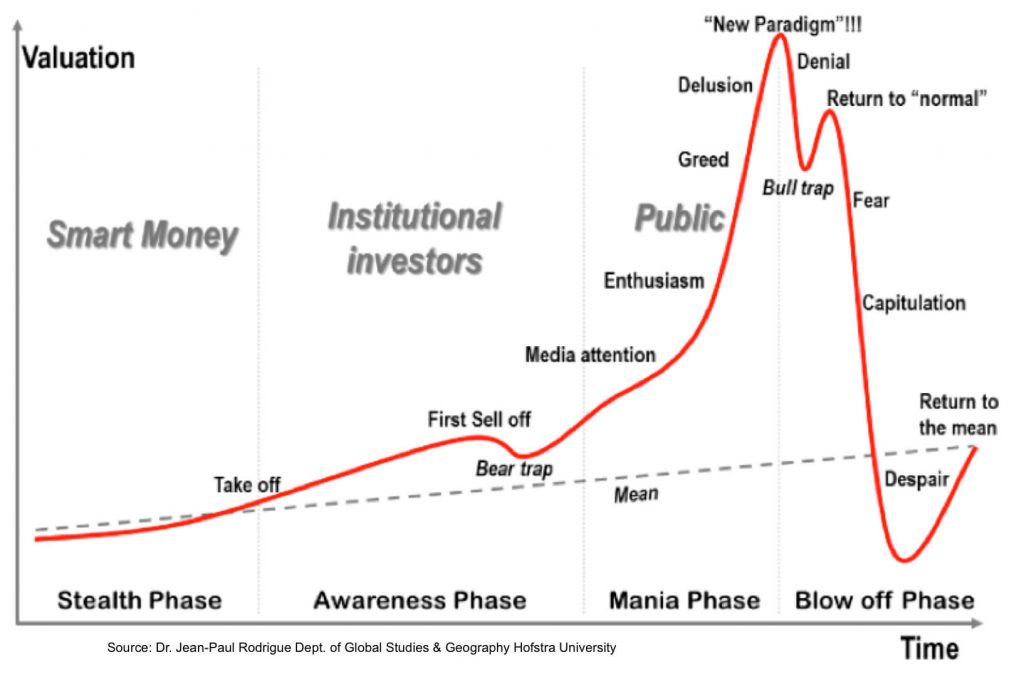

3) Despair

Markets can be very psychological. This is because of a thing in human psychology called “herd mentality”, and markets are just a collection of actors making decisions. Check out this amazing diagram:

The idea here is that individuals might make pretty good decisions, but in groups, they tend to act emotionally. Even as individuals, we can be pretty hopeless, to be honest!

This is a made-up diagram from the internet (it’s so widely used that I couldn’t find out who made it up), and it is a real favourite of mine for explaining things. It’s called “Phases of a Bubble”. I could write a whole blog about it, but for now, I’ll just leave it here and say this:

With respect to the real estate market, the mood feels pretty bad around here sometimes (capitulation?). When the community’s mentality shifts to “despair”, prices might be near the bottom. At that point, there’s a decent chance that the herd has become irrationally negative about prices and prospects for the town. In that way, at that moment, properties could be undervalued vis-a-vis the underlying economic fundamentals.

4) Fewer “For Sale” Signs

It’s human nature to think there are “

For Sale” signs everywhere. Especially when your real estate radar is on. Let’s try this:

If I were to tell you that at no time in the last 3 years has there been an unseasonably large number of homes for sale, would you believe me? No, you wouldn’t! Your real estate radar has been on and, in your mind, there have been listings everywhere.

The truth is though, that there is basically the same number of homes for sale today as there was this time 3 years ago. This correction has, so far, been caused by lack of demand, not oversupply.

If you actually count the signs on your commute, or in your area (or easier, search our website or set up an automatic search), then you will be able to know that inventory is falling. That will be a sign that things are on a path to balancing out.

The tricky bit here will be the seasons. There are always fewer homes listed in the winter than the summer.

5) Peak Foreclosure

A wise man once told me that if someone wanted what’s called a “leading indicator”, they should look at the foreclosure rate. That is, it’s quite possible, that just before prices level out, the fraction of listings in the market which are in

foreclosure could go down.

Here’s a tremendous article that dives into the US housing market and the after-effects of that crisis.

There's No Place Like Home: Housing Market Indicators

Since the financial crisis began, 4.4 million home foreclosures have been completed.27 In April 2013, the number of foreclosures completed—a measure of homes actually lost to foreclosure—was 52,000, a decline of 16% year-over-year compared with April 2012. However, 3.3% of all mortgage holders are still at risk of foreclosure. While the number of homeowners in formal foreclosure processes has declined by a quarter from this time in 2012, there is still a long way to go before those numbers return to pre-crisis levels. Likewise, serious delinquencies—that is, late payments of 90 days or greater—are slowly going down, though at 2.3% of all mortgages they are still at unacceptably high levels. Via thirdway.org

Internally, we track the number of foreclosures/court listings and at last count, there were 87 on the market. That is the highest number we have counted so far, and it has risen by 7 in the last 30 days.

6) More SOLD Signs

Okay, this one is a bit obvious, but it’s tricky because of the seasons and psychology (the number of sold signs you see is probably affected by things like your mood or if you have just had a coffee or not). Are the sold signs you see all represented by a handful of agents (like today), or are they agents you’ve never heard of? If the latter is true, then perhaps it is becoming easier to sell?

7) Other Anecdotal Evidence

If you have friends buying or selling (or ask the internet), are they getting

huge discounts, or are they drying up? Are your friends who were “fence-sitting” getting off that fence and buying?

8) Lots of Consistent Data

You may get statistics from a public source.

If these consistently show higher sales and less inventory, especially if those sales are in traditionally quiet times (fall, winter), or that lower inventory happens in typically high-inventory seasons (spring, summer), this is probably the best sign that the market is starting to balance.

The key here is not to get bogged down in the data: One month isn’t a trend, so you will want to witness several months of this data.

Hope Is Coming

This is an imperfect world full of imperfect information. Our town’s fortunes are tossed around in an ocean of news, generated by the decisions of a handful of people, in palaces and boardrooms thousands of miles away.

While our housing market is complicated and fairly impossible to predict, it is also fascinating and I believe, it can be understood. Even better, there is a lot of observable information out there that can give members of the public a sense of what is going on in our local housing market.

It goes without saying that if you really want to know the Fort McMurray market, then you have to know the data (we have the data) and an expert who actually knows their stuff (we know our stuff). In fact, we have three specialist listing agents and three specialist buyer’s agents hoping to help you.

Final note: Do remember, that most people buy and sell homes at times that fit their lives. The financial side is just one piece of it. Furthermore, a wise man once told me that if you can even pick the right years to buy/sell, then you’re doing incredibly well.

Please feel free to share this article with your loved ones.