Avoiding The Curse of Negative Equity

So, you’re thinking of buying. That really is exciting! But here’s a sobering thought:

We are frequently approached by potential clients who want to sell their homes. Our specialist listing agents meet with them and advise them on pricing and marketing. That is, given the choices they have made in the past (which home they bought, when they bought it, their financing arrangements), what is the best course of action to meet their goal of selling for as much money as possible?

Because home values have fallen so significantly since 2014, all too often, the result of those early meetings is that, realistically, the home is not saleable given the constraints: The mortgage balance is greater than the estimated value (a phenomenon is known as “negative equity”).

The market has forced itself into people’s personal lives: The housing & investment choices those homeowners now have are limited ones; they have a want or a need to sell (e.g. job loss, divorce, etc.), but not the ability to do so.

But what do you, as home buyer today, do to minimize the chances of later finding yourself in that tricky situation? And what can today’s homeowners do to ameliorate their situations? It is an uncertain world, so today’s post hopes to help by answering these important questions and more.

Buy The Right House

If you think there is any chance that you will want to sell in the next 5-10 years, then you need to choose a home that is easily resalable. But what does that mean?

Here’s a guide to help you:

Don’t get me wrong: it’s crucial that you purchase a home that you love and feel at home in, as well as one that fits your wants and needs. But, especially if the planned resale date is in the nearish future, it’s good to at least hold some of these thoughts in your mind to ensure that you invest in a product that won’t pose you too many challenges later.

If you do select a property that might not be easy to resell later, that’s totally okay! Your REALTOR® should be able to price in those challenging elements before formulating the offer with you.

If you secure your home for the right price now, then that will allow you to discount your listing appropriately in the future, too.

More on pricing next...

It’s Not Just About The House

Being able to sell later isn’t all about the home you select.

In fact, the best advice is to make sure the mortgage is low when the time comes to move on. This can be done in four main ways:

Pay the minimum possible price

Maximize the down payment

Pay down the mortgage

Time your purchase like a pro

Let’s cover each of these individually:

1) Price is Everything

We commonly meet potential sellers who tell us that they know that they overpaid for their home back when they bought it.

Today’s home-buyers would do well to perform intensive due diligence when purchasing their home. A great real estate agent will ensure this is done: you will know the value story (and deeper story) of the property, prior to purchasing.

Often a great price is achieved through negotiating a significant discount.

But not always...

Different real estate agents systematically list homes for more competitive prices than others. If a home is listed on or below value, coming in with a low offer and staying stubbornly low may lead to an unbelievable deal, but the chances are that a good listing agent will defend the price and ultimately, someone else will pay more than you for the property, even in a buyer’s market. So it’s best to go into those negotiations with lower expectations.

The key is to focus less rigorously on achieving some arbitrary discount (“I want a certain discount off the list price”), but on the difference between value (estimated by your agent) and the price you pay. Snagging $20,000 or so value this way will result in lower mortgage payments and a significantly lower mortgage balance when it comes time to sell. This could make all the difference 5 or 10 years from now.

2) Save First. Then Buy.

This is a really tough one. Saving is an elusive goal for many of us, especially in the light of the ongoing downturn (lower incomes) as well as the stubbornly high cost of living in Fort McMurray.

Homes are still expensive in Fort McMurray (in nominal terms, versus the rest of Canada), but if your income is high, then they may, in fact, be cheap for you. Either way, saving up for a chunky down payment might be a prudent goal. But why?

Saving beyond the minimum down payment can have a significant impact on your ability to sell later. Potential sellers that we meet who are not in a position to sell are often the people who put 5% or 0% down when they purchased.

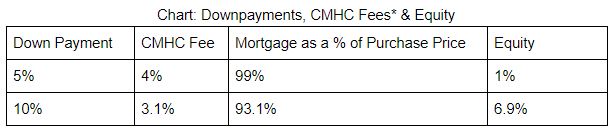

In addition, in Canada, when you put less than 20% down on a mortgage, then a fee from the federal government (CHMC) is levied and added to your mortgage.

These fees have gone up a lot, to the extent that today, if you put down 5%, the fee is 4%! This will leave you with only 1% equity the day you move in. In part because of the lower fee, moving to a 10% down payment will give you 6.9% equity on possession day instead of 1%. This will help when it’s time to move on. Confused? See the chart below:

*See the CMHC website for more info.

*See the CMHC website for more info.

As REALTORS®, our role is to offer only a basic introduction to these issues. Talk to your financial advisor about the timing of your savings & investments for quality, case-specific advice.

3) Shooting for “Mortgage Free”

Talk to your mortgage advisor about options to pay your mortgage down over a smaller amortization than 25 or 30 years. This will make scheduled payments larger and result in a lower mortgage balance when it’s time to sell. Perhaps there are pre-pay options to achieve the same thing?

Here’s a wonderful article from Canadian Living that details plenty of these options and more:

5 ways to pay off your mortgage faster

2. Round up your mortgage payments

Make no mistake: Every dollar counts when it comes to paying off your mortgage. The quicker you can pay off your loan, the more you will save in interest. A painless way to make your mortgage disappear faster is to round up your mortgage payments. So if your accelerated bi-weekly mortgage payments are $543, consider rounding up to $600 instead. The extra $57 will do wonders for your mortgage and chances are you will barely notice a difference in your monthly budget.

If you receive a raise, instead of increasing the cost of your lifestyle in the short term, consider throwing the extra amount you make onto your mortgage instead. read more...

We have found that today’s sellers often have negative equity, in part because of the longer amortizations (35 and 40 years) that were common in the past.

On the flip side, a lot of our successful seller clients have either paid down their mortgages or saved money to one side in case of this “rainy day” scenario. These funds can be used to pay off the mortgage when it’s your time to sell (this is a deeply personal decision).

In a similar vein, your choice of home budget will impact your ability to make extra mortgage payments, etc. A conservative choice today can lead you to be able to successfully “move up” into your dream home tomorrow.

I am conscious that a lot of this advice might seem a bit “boring” and that I sound a lot like my Dad (he’s British). But spending time advising buyers and sellers in Fort McMurray over the last 3 years has caused us to become even more conservative in our advice.

4) Buy Low, Sell High

Okay so this sounds impossible, but it’s not entirely silly so please bare with me. Note, these are my opinions:

Is it possible to predict the future? Maybe for the next few months. Not in the long run, no.

Will prices be higher 5-10 years from now? Unknowable. What’s your view of the future?

Are prices lower than in the past? Yes

Are prices falling now? Yes

Will prices fall forever? No. All markets eventually balance.

What determines the short-run future of prices? Supply and demand.

What are they saying now? Supply is in line with previous years at this time of the year. Demand is still reduced approximately 40-50% versus the boom years.

Timing purchases and sales is, to some extent, a fool’s game, especially when talking about your primary residence (typically people buy for personal, not financial reasons), but let’s say you want to give it a go...

Imagine: Prices are falling (it’s a buyer’s market) and you have a savings goal of 10% to 20% down anyway. Let’s say your real estate agent gives you guidance that the market is not showing imminent signs of rebalancing yet. Perhaps there is an argument for waiting? This will likely depend on your view of the world and of the future, as well as why you are buying (can you wait?).

It does go without saying, however, that the primary reason why potential Fort McMurray sellers ended up in an uncomfortable negative equity position is that they had the misfortune of bad timing...

Very few people saw the lasting structural changes in the oil market coming. But those changes (and other causes) have led to a multi-year demand depression which has, in turn, led to the long-term slide in prices. See our blog about the Fort McMurray real estate crash to learn more.

Timing is almost impossible in the big scheme of things (you’ll do well to pick a good year), but when prices are adjusting rapidly, buying a month or two earlier (or later), can have a material impact on your ability to sell in future. You want to find a buyer’s agent who is an amazing REALTOR® who can give you quality, honest, unbiased advice.

A Bright Future For You

Buying a home is pretty much the coolest thing you can do. Super fun. But as we all know, life is not always sunshine and lollipops.

Hopefully, today’s buyers will find some of these ideas helpful. It is an uncertain world, and prices are still falling, but we have systematically found that the people who make these choices tend to be more likely to be able to sell when their time comes. A lot is out of your control, but the biggest determinants seem to be peoples’:

a) Timing (partly in your control?)

b) Ability & willingness to save (partly in your control)

We wish everyone out there the best of luck as we navigate through this downturn as a community. Fort McMurray is hard-working and caring. For me, those are the things that make this community my forever home.