Buying Investment Properties in Fort McMurray

It’s a question we’re getting asked often these days (no one asked for about three years). The answer to the question is also relevant to potential sellers. So read on

...

If you are thinking about becoming a real estate investor in Fort McMurray, here are three steps for maximizing your chances of finding some kind of enlightenment:

- Understand How Risky This Is

- Numbers Are All That Matters

- Invest (Don’t Speculate)

Firstly, I’ll go through these three concepts, checking them off, one by one.

Then I’ll share some conclusions I drew today while seeking out the best Fort McMurray real estate investments on behalf of a client. I’ll compare the returns that were estimated today to what they might have looked like three years ago.

With any luck, this will help you determine if now is a good time for you to make an investment or not, or whether to sell or hold properties in your existing portfolio.

1) Understanding How Risky This Is

It’s risky.

Your job is here.

Your expensive primary residence is here.

And “here” is ostensibly a one-horse town.

Beyond market risk, there are risks with foreclosures, risks at the condo management/board level, and the risk that managing your investments can become a full time job (I’m only half kidding!). Our role as buyer’s agents is to help identify those risks and help you understand them and protect yourself as best as possible.

Financial advisors have told me that they think there’s a lot to be said for diversification. They might advise you to have an investment property in BC, one in the US, and one in Montreal, for example. But let’s say you are a risk taker, or you have those properties already. I get it, you want to buy an investment property in Fort McMurray.

You understand that this is risky. Step one ✔️

2) Numbers Are All That Matters

First-time investors often think a little bit like consumers. It’s natural (after a misspent youth watching HGTV) to picture yourself in

condos/homes and start ordering the listings in terms of how happy you would be to live there...

...it’s a better idea to avoid this trap.

For me, when talking about an investment, there’s one number that matters: Cash On Cash Return (Coc).

This is the holy grail of many real estate investors. That is, at any given level of risk, which investment is anticipated to deliver the highest percentage of the initial outlay back in a given period of time (usually one year)?

The proper definition can be found in the Mashvisor article below, as well as a number of other measures of investment efficiency:

Cash On Cash Return (CoC)

h/t mashvisor.com A third widely used metric for determining the profitability of a real estate investment is the cash on cash return, or the CoC return. Unlike the cap rate, the CoC return varies with the method of financing, as you will see in the formula in a bit. The CoC return measures the annual return on your investment based on the NOI and the total cash investment.

CoC return = NOI/Total cash investment

It doesn’t so much matter how you estimate the efficiency of your investment, so much as that you estimate it somehow! What you base all your decisions on is return.

It’s kind of freeing to know that, unlike the purchase of your forever home, this transaction is only about money; knowing that is your second step in the right direction. ✔️

3) Invest (Don’t Speculate)

This town, just like any other (but in a different way more than any other) is full of a) hope and b) despair. You’re going to want to do neither. Here’s what I mean:

Unless you have an incredibly strong argument that prices are going to go up, don’t count on it. According to the absorption rate, and the new listings to sales ratio, we are now in a balanced market. We are not aware of market rents rising. In economics, in a market which is in equilibrium, the most reasonable expectation of future prices is today’s price so I would caution against factoring any appreciation into your investment return calculation.

If you are buying with an expectation that prices will be higher in the future, then you are speculating, not investing, and you’re doing so by leveraging your large investments in a high-risk market. Woah there, Nelly!

In summary, all that matters, in my opinion, is your investment return from rent (after costs) over time, and not price appreciation.

So you’re ready to assume zero price-growth? Check number 3. ✔️

CoC Now Vs. 2 Years Ago

Today was a fun day.

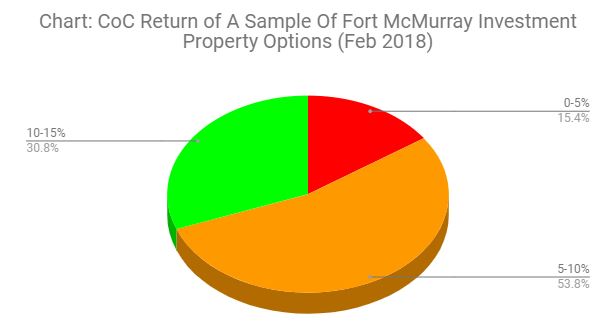

Thirteen properties were visited, assessed, and their CoC returns were estimated. I won’t go into too much gory detail as to how the client calculated CoC. Instead, let’s check out the cool pie chart that resulted:

As you can see:

- 2 of the properties had poor anticipated returns (15.4% of properties had returns of less than 5%)

- 7 of the properties had reasonable anticipated returns (53.8% of properties had 5-10% returns)

- 4 of the properties had good anticipated returns (30.8% of properties had 10-15% returns)

In a nutshell, today, decent returns are there if you know where to look for them (remember, most of these are risky investments so you’re going to want 10%+ in my opinion).

Over the winter of 2014/2015, rents fell dramatically due to unemployment causing less demand and therefore a high vacancy rate. By the end of the winter, rents were down and have stayed down, but residential real estate prices had only just begun to adjust downwards.

My thought is:

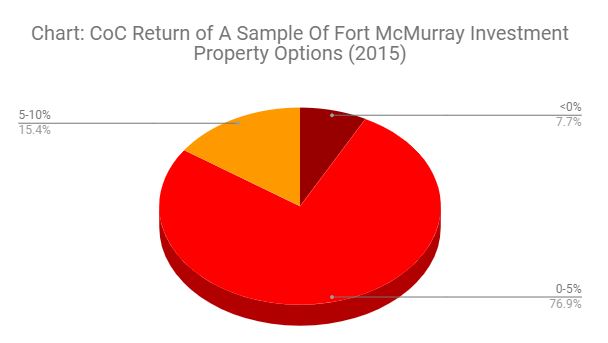

“Prices have changed dramatically since 2015, so what WOULD this pie-chart have looked like in early 2015 given the old prices? Would it have been a good time to buy an investment property?” - My thought

As an experiment, I just took a look at what comparable properties were roughly selling for in early 2015, and popped those numbers into the CoC spreadsheet. Here is the resulting pie-chart:

As you can see:

As you can see:

- 1 of the properties had a negative anticipated return (7.7% had returns of less than 0% return)

- 10 of the properties had poor anticipated returns (76.9% had 0-5% returns)

- 2 of the properties had reasonable anticipated returns (15.4% had 0-10% returns)

What’s more, these poor returns are a prime candidate for having caused value changes in properties over the last three years. Investors decided not to buy at the same time that many consumers

decided to rent instead of jumping in.

Conclusions

For most of the last three years, residential real estate prices have been adjusting down due in large part to lower market rents (rents adjust much faster because prices of real estate are “sticky”). During those three years, most of the time, for most investors and most properties, it has not made sense to buy or hold investment properties.

Today, prices are lower, and there are now options out there that are anticipated to give good returns, based on conservative assumptions (e.g. no price growth).

Is it “time to buy”?

Well, I think that depends a lot on your personal situation and view of the future (what about, for example, interest rates?).

However I would go so far as to say that it’s not “not time to buy” based on the analysis from today’s journey.

The experiment also gives weight to the anecdotal evidence we have witnessed lately: That investors are once again sniffing around more so even than they were six months ago. Investor demand supports prices, so it’s a further piece of evidence that we have entered a balanced market.

If you are thinking of buying or selling any type of property, we would love to help you with tailor-made advice just for you and your family. Thanks for reading!